Hint: 3x doesn’t always mark the spot.

Exec summary

If you Google LTV:CAC, you’ll find a lot of advice saying you need your metric to be at least 3x, but you’ll find less guidance telling you why. The why matters — depending on your operating expense (“OpEx”) composition, 3x could lead to a profitable SaaS company, or 3x could lead to bankruptcy.

The key to determining a healthy LTV:CAC ratio for your SaaS company is to consider the relative investment your company is making into Research & Development (“R&D”), Sales & Marketing (“S&M”), and General & Administrative (“G&A”) operating expenses.

As you’ll learn below, 3x LTV:CAC ratio is high enough only if S&M makes up at least 33% of your total OpEx spend.

A quick refresher of LTV:CAC and why it’s important

Comparing lifetime value (“LTV”) to customer acquisition cost (“CAC”) results in the LTV:CAC ratio, which is one of the most important metrics for SaaS companies. It is a unit economic metric (describing the unit economics of either a customer, or as I like to think about it in the case of a land & expand business, $1 of ARR) that encompasses all aspects of your P&L and tells you whether your SaaS business can be profitable.

Unit economics are especially important for SaaS companies because of timing. Specifically, the difference in timing between cash outflows incurred to acquire revenue from a customer that happen now (i.e. CAC), and the cash inflows from that customer’s revenue that happen over a period of time in the future.

In order to make a meaningful comparison between the immediate cash outflows and the periodic future cash inflows, we need to convert the cash inflows into a single point in time value. The LTV formula does just that — it turns all of our future customer cash inflows (on a gross profit basis, so adjusting for cost to serve that revenue) into a present value figure. I also suggest including the impact of non-recurring professional services profit/loss in LTV. I won’t go into detail in this post on how to calculate LTV, but you can read more here.

The resulting LTV:CAC ratio tells us about the profitability of our business.

Making sense of LTV:CAC results

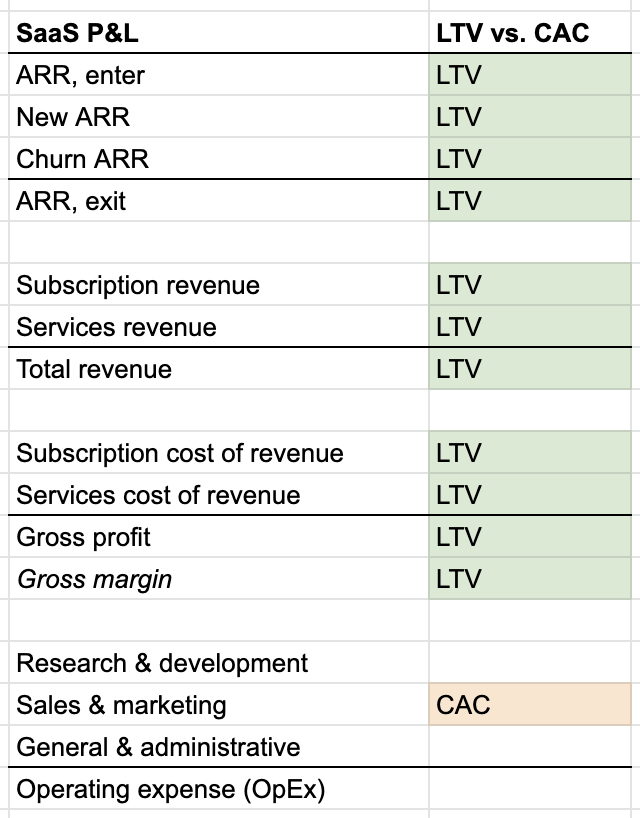

We’re trying to understand profitability, so let’s look at the SaaS P&L (like a regular P&L, but starting with the ARR bridge). The LTV formula is comprised of subscription gross profit dollars over an estimated period of time plus professional services profit/loss. As you can see below, these components encompass the top portion of the P&L through gross profit. Similarly, CAC is represented by S&M expense, which is a component of our OpEx.

So at the most basic level, LTV:CAC is a comparison between gross profit and S&M expense.

Okay, the theory makes sense, now let’s add some numbers.

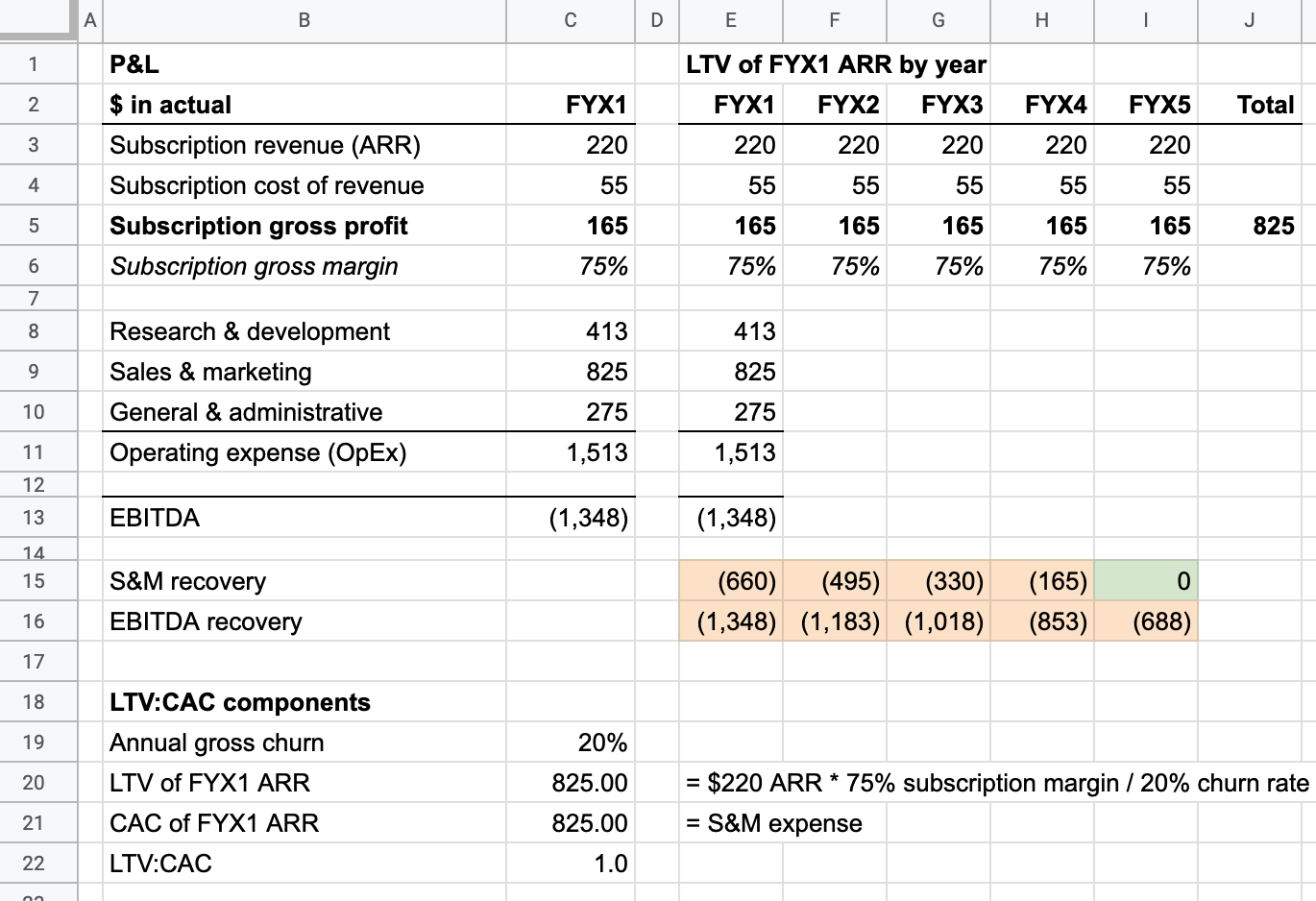

Consider an example fiscal year FYX1 in which our company sells $220 ARR. And we incurred $825 in S&M expense to acquire that ARR. We have a subscription gross margin of 75%, an annual churn rate of 20% (1/20% = 5 year LTV), and we break even on our professional services ($0 of professional services gross profit so no impact to LTV):

As you can see, the resulting LTV of that $220 ARR is $825 (calculated two ways: (1) using the perpetuity formula on row 20 and (2) summing the 5 years of gross profit on row 5) and CAC is also $825. So the LTV:CAC ratio is 1.0x. The S&M recovery line on row 15 also illustrates how the gross profit generated from our FYX1 customers during their lifetime (in this case $165/year for 5 years) will pay for exactly the cost that we incurred to acquire them through year 5, after which that ARR churns.

From looking at the EBITDA recovery line on row 16, you can see that our customers are not funding the $688 cost of our R&D functions (that are building our product), nor our G&A functions (that are billing and collecting from customers, keeping the books, etc.).

What does the LTV:CAC ratio need to be to ensure our customers fund our operations?

The answer comes by comparing the S&M expense to R&D and G&A.

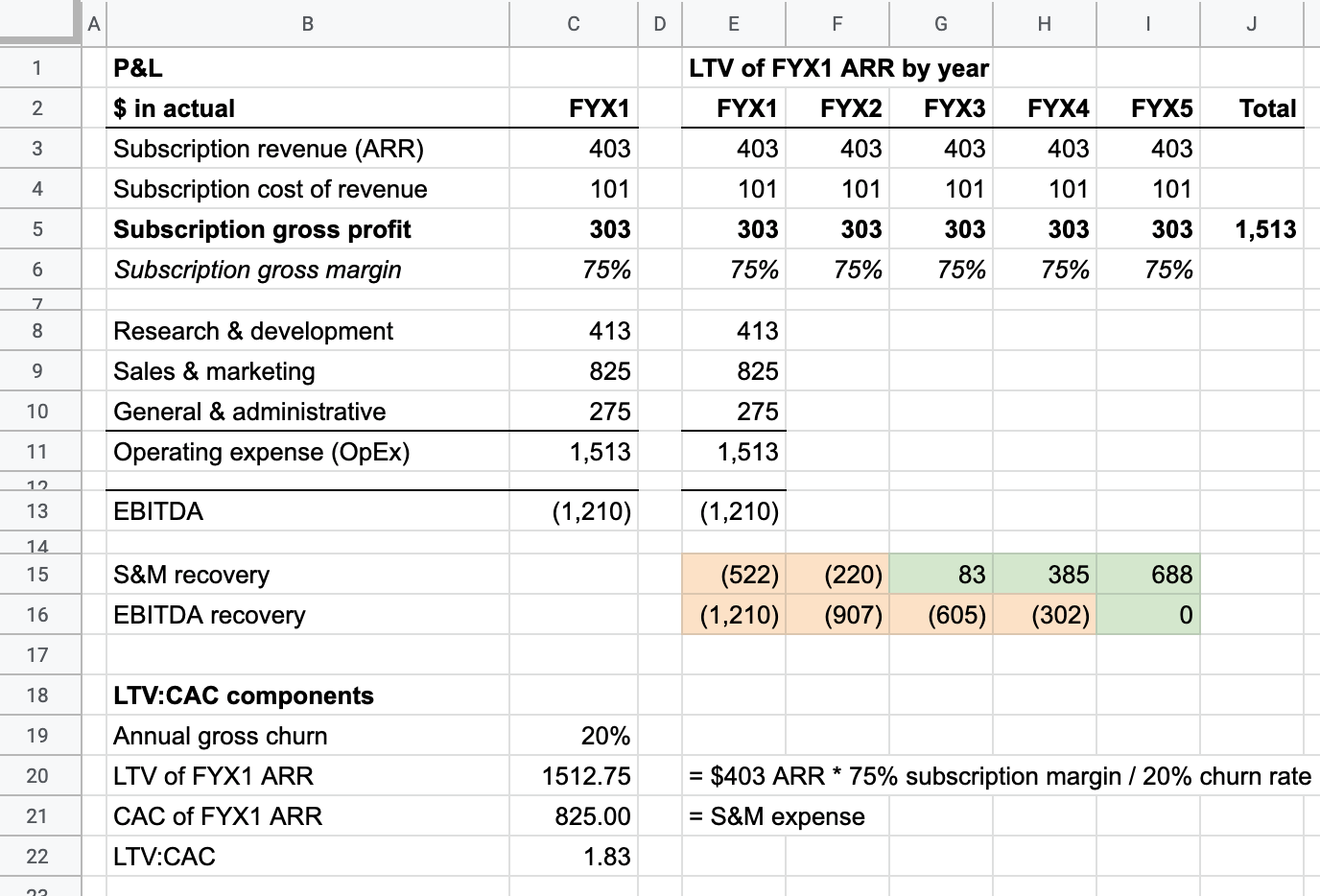

In this example, S&M expense comprises 55% of our total OpEx. We know that an LTV:CAC of 1x means our LTV covers just our S&M expense. So if we wanted the LTV from the customers we signed in FYX1 to cover all of our OpEx we incurred in FYX1, we would need an LTV:CAC ratio of 1.83x (1 / 55%). Achieving 1.83x LTV:CAC would mean that our unit economics are break even — the gross profit we generate from our customers funds our business’ operations. We won’t generate a profit, but we also won’t generate a loss.

Said differently, if we’re above 1.83x then the unit economics are profitable. And if we’re below 1.83x then the unit economics are unprofitable and (ignoring the impact of timing) we will be funding our business with other non-customer sources of cash (e.g. equity or debt). All else equal, we would have needed to acquire $403 ARR in FYX1 to have achieved profitable unit economics:

This also shows that we have a payback period of just under 3 years, as S&M recovery goes from negative to positive in FYX3.

While 1.83x+ means that we’ll eventually be profitable, if you recall the first point on timing, we incur R&D, S&M, and G&A cash outflows now while we only recover those costs via customer cash inflows over time. This is why SaaS companies that are growing fast and acquiring a lot of ARR are typically more unprofitable in the near term, but if the unit economics are in the green it often makes sense to incur the short term losses.

How to think about a changing OpEx composition

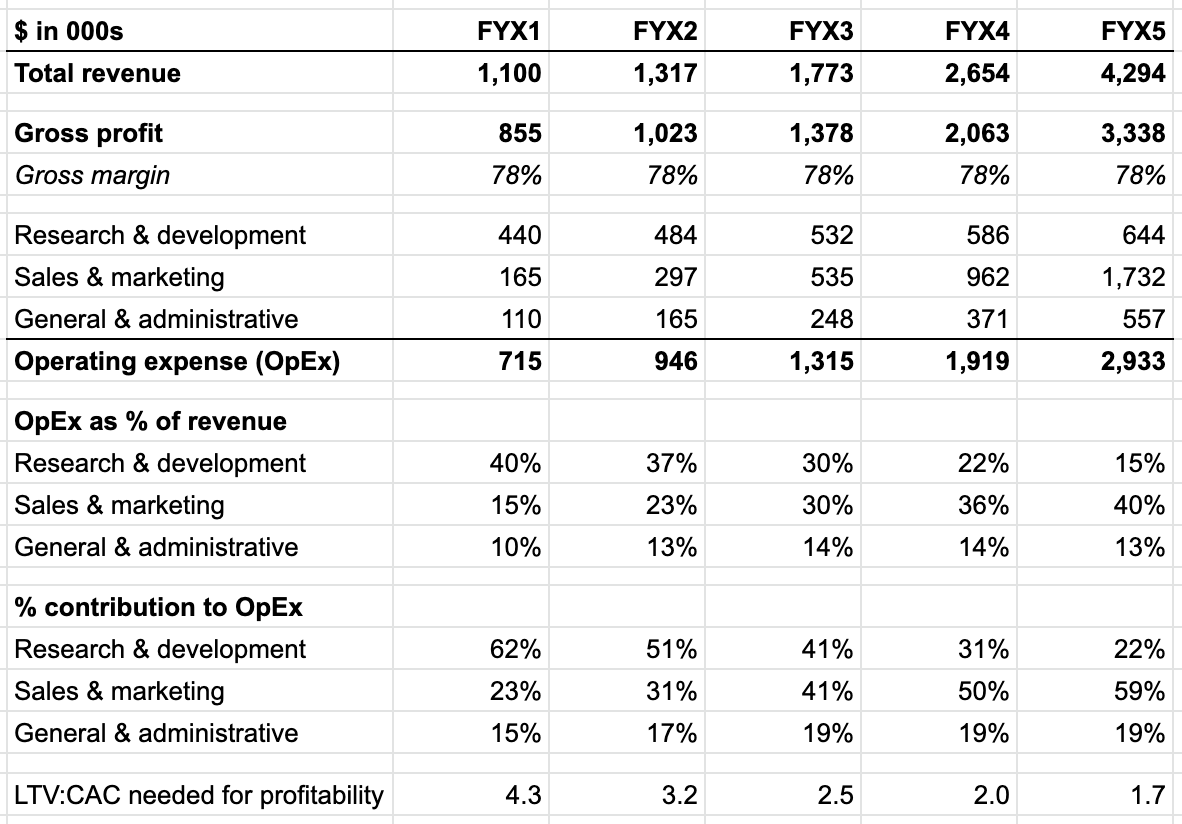

Your OpEx investment will change throughout the life of your SaaS company. At the beginning it is common to be heavily invested in R&D (relative to S&M and G&A) to build product. Once you achieve product-market-fit and have figured out your repeatable, profitable go-to-market motion, you’ll likely shift more investment into S&M as you’re selling your product. Here’s an example shift in OpEx investment over time for a SaaS company:

The LTV:CAC required for profitability is much higher in FYX1 when the company is mostly invested in R&D. As the company shifts into more S&M investment, the LTV:CAC ratio required for profitability drastically declines. This table illustrates a few points:

- If your LTV:CAC doesn’t produce profitability in the early years when you’re heavily invested in R&D, that doesn’t mean you will never achieve profitability. In fact, in the early year(s) LTV:CAC may not accurately reflect the mid/long-term ability of the company to become profitable and doesn’t need to be a focus. Once product market fit is achieved, considering LTV:CAC will help inform you on whether you have a profitable growth model that is ready to scale.

- Your LTV:CAC required for profitability will change throughout the life of your company. After taking into consideration point 1 above, a good goal is that your LTV:CAC ratio is above the profitability threshold based on your OpEx structure in each year. The higher above that threshold, the faster you’ll reach profitability

Time horizon limits

Another way to look at LTV:CAC is a time-horizon based view. What is the LTV:CAC ratio if we limit the LTV to X years? And will my customer revenue fund my company’s operations during that shortened timeframe? I’ve seen this methodology used with growth equity/PE investors as they try and determine the return on investment over the period of time in which they are considering holding your company before exiting.

Let’s say a growth equity investor wants to invest in your SaaS company and wants an exit in 3-5 years. Rather than using your regular churn rate in the LTV formula, they may use 33.3% to force a 3 year LTV.

Photo by Aperture Vintage on Unsplash

[…] What should your LTV:CAC ratio be? […]

LikeLike